Global trends in the development of aircraft manufacturing enterprises. Russian aviation market New projects by Bombardier

The transformation of the economy is accompanied by a transition from transnational integration to transcontinental integration, which manifests itself for the world aircraft market in the emergence of prerequisites for the disappearance of such concepts as the "American/European/Russian aviation industry": the capacities of the Eastern European aviation industry are used in the production of American aircraft; the Chinese aircraft manufacturer AVIC cooperates with the European concern Airbus and the American corporation General Electric, etc. Any attempt to close in on a national scale today has no prospects. This determines the primary importance of the influence of global factors on the development of an individual company. Therefore, the modern world civil aviation market, on the one hand, reflects the main global economic trends of today, but on the other hand, it has its own development specifics.

Trends in the development of the world aircraft industry are simultaneously covered in the studies of aircraft manufacturing corporations that have their own research centers, and in studies conducted by scientists as part of their activities in scientific institutions. Among the main studies that form the basis of the strategies of aircraft manufacturing corporations are "Global Market Forecast" from Airbus, "Current Market Outlook 20122031" from Boeing, "Market Forecast" from Bombardier, Worldwide Market Forecast 2014-2033 from Japan Aircraft Development Corporation and some other. The International Civil Aviation Organization (ICAO) also regularly publishes the results of its own research (eg "Airplane Outlook"). Partially based on such forecasts, the prospects for the aircraft industry are highlighted in the scientific research of J. Wensvin and A. Wells .S. Sokolova, M.V. Boykova, S.D. Gavrilov and N.A. Gavrilicheva A. Khatypova and T.T. Khalilova, T. Boetsha, T. Vigera and A. Vitmera, Yu. Prikhodko and other authors.

First of all, the existing studies note the transformation of the market structure of the aircraft industry and, accordingly, analyze the strategies of the leading market agents. However, at the same time, certain features are distinguished that characterize changes in the aircraft industry, and the available forecasts for the development of the aircraft industry market are built mainly on the basis of forecasting the demand for aircraft and the study of the factors influencing it, and do not take into account the general direction of socio-economic development as a whole. That is, we can talk about the lack of an integrated approach in the analysis of the current state and changes in the industry, which significantly reduces the reliability and completeness of forecasts. Given this, there is a need to systematize individual manifestations and form a holistic view of changes in the global aircraft manufacturing market. At the same time, the formation of a holistic view of changes in the global aircraft manufacturing market, from our point of view, provides (Fig. 3.4):

firstly, analysis of the structure of the global aircraft manufacturing market, determination of segmentation criteria and main market agents, generalization of the main trends;

secondly, the analysis of external factors influencing the development of the aircraft industry in the context of quantitative and qualitative parameters;

thirdly, the analysis of the behavior of market entities, the definition of business organization methods inherent in market leaders.

Fig.3.4. v Tasks of researching changes in the global aircraft manufacturing market

Segments and structure of the aircraft industry market

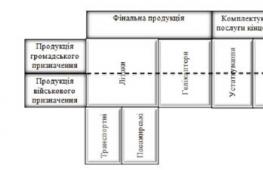

The modern structure of the aircraft manufacturing market has a matrix character: on the one hand, there is a distribution, on the one hand, into two sectors - the production of final products and consumer services (spare parts, components, services), on the other hand, each of these sectors is divided into sectors of civil and military products (Figure 3.5).

Several companies can be distinguished in the military aircraft market: Boeing - approximately 22% in the world military aircraft industry in 2011, Lockheed Martin - 21%, Northrop Grumman - 11% (the combined share of US companies in the world military aircraft industry is 54%), Eurofighter - about 11%, EADS - 10%, Dassault - 4% (the total share of European Union companies in the global military aircraft industry is 25%), the share of Russian companies is 20.6%. At the same time, there is the creation of a common Anglo-Saxon transatlantic defense market with a powerful diffusion of the military-industrial complexes of countries, and on the territory of the European Union - the formation of a single defense market within the countries included in it.

Fig.3.5. v

Among the specific trends in the development of the military aircraft market, the following can be noted:

In countries that are developing, instead of buying new military aircraft, there is an increase in demand for the modernization of existing weapons with the provision of appropriate operational support;

Economically developed countries are getting rid of technically obsolete aircraft, stimulating its sale by transferring rights to licensed production, assistance in establishing a service infrastructure;

The formation of demand for military aircraft depends on the political and economic climate on the planet and the strategic relationship between countries.

The biggest obstacle to the analysis of the military aircraft market is political bias, which manifests itself in the secrecy or lack of reliable information about the characteristics of the latest technology and contracts. Taking into account these factors, the ratio of the civil and military aircraft market (the total share of the military aircraft industry is about 40% of the world's aircraft industry, and about 20% in the final product), as well as the trend of borrowing civil and military aircraft manufacturing technologies, we are focusing on the study of the civil aircraft industry in the world.

At the same time, in the civil aircraft industry, the output of final products is distributed between aircraft and helicopters as 88-90% / 12-10% in favor of aircraft. Therefore, we will focus our analysis of trends in the aircraft manufacturing market on the example of the civil aircraft manufacturing market and will follow the steps shown in Figure 3.6.

Fig.3.6. v

In order to characterize the global civil aircraft market, given the significant differentiation of aviation technology, it is necessary to consider the criteria for its segmentation.

Most often, the civil aircraft market, depending on the type of fuselage and flight range, is divided into the following segments: the market for medium and long-haul wide-body aircraft, the market for medium- and long-haul narrow-body aircraft, the market for regional and local aircraft (Appendix B).

This type of market segmentation is rather conditional and can be modified in different studies - smaller segments are additionally allocated or a larger hem is used.

Also, three criteria are used to segment the aviation market: the type of aircraft power plant (turboprop, jet), the purpose of the aircraft (passenger, transport) and passenger or cargo capacity. Therefore, in order to form a more complete picture of the aircraft manufacturing market, in the future we will use mixed segmentation for market analysis, which is presented in Appendix D.

The development of segments of the civil aircraft market is related to the range of transportation, therefore, we will characterize the distribution of the world passenger traffic by type of aircraft and flight range (see Figure 3.7). The main passenger traffic falls on narrow-body aircraft that operate on routes from 500 to 4500 km, reaching the ASK indicator (Available Seat Kilometers - passenger-seat-kilometers) on lines from 1000 to 3500 km in the amount of 300 to 750 million passenger seats-kilometers. Turboprop aircraft mainly operate on lines up to 1500 km, the same length is the main one for regional aircraft - on lines up to 1500 km, the passenger traffic is more than 100 million passenger seats per kilometer. Passenger transportation on lines of 4000 km or more is carried out mainly by wide-body aircraft. It should be noted that routes up to 4500 km account for about 65% of passenger traffic.

Fig.3.7. v

In terms of passenger capacity with a transportation distance of up to 1000 km, the most common are airliners with a capacity of 120-169 seats, from 1001 to 2000 km - 120-169 and 170-229 seats, from 2001 to 4500 km - 120169, 170-229, 230-309 and 310-399 seats, more than 4500 km - 230-309, 310-399, 400-499 and 500-800 seats (Figure 3.8).

Fig.3.8. in (built from data)

The structure of the fleet of jet passenger aircraft in 2013 is shown in Fig. 3.9-10, from which it can be seen that the largest share in the composition of aircraft is with a significant predominance of aircraft with a capacity of 120-169 seats (51.22%), in second place - aircraft with a capacity of 60-99 seats (19.39%).

Analysis of the dynamics of the fleet of turboprop passenger aircraft in the world for 2000-2013. (Figure 3.11) shows an overall decline in the use of turboprop passenger aircraft, which is most affected by the segment of aircraft with a capacity of 15-39 seats (almost 30% in 2013 compared to 2000) and is slightly offset by the growth of the segment of aircraft with a capacity of more than 60 places (almost 12% in 2013 compared to 2000).

Fig.3.9. in (built from data)

Fig.3.10. in (built from data)

Fig.3.11. in (built from data)

This is due to the appearance in the second half of the 1990s-early 2000s. jet aircraft with less than 50 seats, which are more economical than the corresponding turboprops. As a result, the structure of the turboprop passenger aircraft market in 2013 (see Figure 3.12) consists of three segments: aircraft with a capacity of 15-39 seats -51.66% (68.62% in 2000), 40-59 seats - 22.56% (23.9 in 2000), more than 60 seats - 25.79% (7.49% in 2000).

Fig.3.12. in (built from data)

Let's analyze the distribution of types of airliners in the regional context (Fig. 3.13 and Fig. 3.14).

Fig.3.13. in (built from data)

As can be seen from Figure 3.13 and Appendix E data, regional jets are most common in North America (53.62% of the total number of regional jets) and Europe (16.91%). Narrow-body jets are most in demand in the Asia-Pacific region (29.11% of the total number of narrow-body jets), North America (28.3%), Europe (22.8%). Wide-body jets are more used for transportation in the Asia-Pacific region (37.18% of the total number of wide-body jets), Europe (20.99%), North America (16.66%).

Turboprop passenger aircraft (figure 3.14 and Annex E data) are generally most operated in the Asia-Pacific region (25.44% of the total number of turboprops). At the same time, North America (30.68% of the total number of turboprop aircraft with a capacity of 15-39 seats) and the Asia-Pacific region (22.61%) are leaders in the local transportation market, in the regional market in the segment of aircraft with a capacity of 40-59 seats, Asia-Pacific Pacific region (23.92% of the total number of turboprop aircraft with a capacity of 40-59 seats) and CIS countries (22.15%), in the segment of aircraft with a capacity of over 60 seats - Asia-Pacific region (32.45% of the total number of turboprop aircraft with a capacity of over 60 seats), Europe (26.8%) and North America (16.61%). To explain this spread of jet and turboprop passenger aircraft, it is necessary to analyze the economic and other specifics of the regions of the world.

Fig.3.14. in (built from data)

Let's analyze the trends in the development of the jet cargo aircraft market (Fig. 3.15).

Between 2000 and 2013, the total number of jet cargo aircraft decreased by 4.5% and the structure of this market changed. Thus, in 2000, 39.67% of the total were narrow-body cargo aircraft and 40.01% were medium wide-body cargo aircraft. After a sharp increase in the use of narrow-body cargo aircraft in 2005 to 50.28% of the total in 2013, a proportional market structure was established (approximately 33% each segment).

Fig.3.15. in (built from data)

In addition to the economic factors that determine the use of cargo aircraft, it is necessary to take into account the current practice of converting passenger aircraft into cargo aircraft. So, about 50% of the cargo aircraft operating in the world today were converted into cargo ones at one time. The conversion of passenger aircraft begins after 10 years of operation, since the peak use of passenger aircraft is 15 years. After conversion to the point of disposal, converted cargo aircraft operate for about 25 years. Since 2003, there has been a trend towards a reduction in the conversion practice (Figure 3.16).

Fig.3.16. in (built from data)

Regionally, analysis of cargo aircraft operation in 2012 (Figure 3.17) shows that three regions account for the largest share of cargo aircraft use: Asia-Pacific (29%), Europe (26%) and North America (25%) .

Fig.3.17. in (built from data)

Let's compare the movement of freight and passenger traffic in the regional context. As can be seen from Figure 3.18, the operation of cargo and passenger aircraft by regions of the world has a similar distribution, which allows us to assume the influence of the same factors on these markets.

Fig.3.18. in (built from data)

Let us summarize the analysis of the development of the aircraft manufacturing market segments (final products) by simultaneously determining the distribution of segments by manufacturing companies and aircraft type (Fig. 3.19).

At present, two conglomerates Boeing (SELA) and Airbus S.A.S. (European Union) compete on the market of long-haul airliners (25.2% of the global aircraft manufacturing market), with a combined market share of more than 90%; in the regional aircraft market - Bombardier (Canada) and Embraer (Brazil) with a combined market share of about 78%. The production of the CIS countries, including Ukraine, reaches about 2% of civil aircraft.

Fig.3.19. c (end product 2010-2011 according to data)

Thus, the modern world fleet of civil airliners consists of jet and turboprop aircraft, which has a wide segmentation. Each type of aircraft, through its technical and economic characteristics, has its own market niche and a certain area of competition (flight range up to 1000 km; passenger capacity 60-99 seats). In general, jet aircraft are the most common in 2013. Turboprop aircraft are being phased out of service due to aging and are not being replaced in adequate numbers by new ones, but it is impossible to speak of a decline in this market segment. According to the results of the analysis of the operation of aircraft in the regional context, it is impossible to unambiguously determine the predominance of one or another type of aircraft, therefore, an explanation of the general dynamics and distribution of traffic by regions of the world requires studying the factors influencing the development of the aircraft manufacturing market. At the same time, it should be noted the uneven development of the aircraft industry by region.

In the context of the decline in which the world economy is located, infrastructure sectors, in particular, transport, have suffered quite a lot. Enough has been written and said about the global crisis in freight transportation, especially by sea, and here the situation in Russia differs slightly from the global state of affairs, at least in terms of the dynamics of operational indicators.

Revenue from passenger and cargo air transportation

Source: IATA

The turning point, by and large, came during the financial crisis of 2008 - since then, global trade has still not been able to confidently return to the previous state of vigorous growth, limited to a sluggish recovery, but passenger transportation, with the restoration of disposable incomes of the population, was able to - The industry has experienced a real take-off in the last five years.

Dynamics of volumes of passenger and cargo air transportation

Source: IATA

With regard to civil air transportation, however, the situation is noteworthy in that the situation on the domestic market with the onset of the currency crisis diverged from the world trend as a whole by almost 180%. There are several main reasons for this, and this article will be devoted to their consideration, together with a general overview of this market, covering, without exaggeration, almost the entire planet.

The history of civil aviation dates back more than a century. Since the First World War, it has experienced several idiosyncratic intra-industry technological patterns before taking the direction of development that most airlines are now following. The first passenger monoplanes were small, carried 7-10 passengers each, and were mostly variations on the theme of military aircraft of those design bureaus in which they were created. In the 1930s, the trend was reversed with the advent of the DC-3, the most massive passenger aircraft in history, which, in turn, served the armed forces well. The 50s were marked by the appearance of the first serial jet liners, which by the beginning of the 70s, with the active growth of transcontinental passenger traffic and the emergence of more powerful engines, led to a period of megalomania in the industry, when manufacturers tried to build, and airlines, in turn, to operate as Larger aircraft, accommodating several hundred people, were possible, since the Boeing-707 and other aircraft of this type used at that time could no longer cope with the flow of passengers on busy routes. The successful introduction of such liners was prevented by the oil crisis, which made the use of large and uneconomical aircraft unprofitable, but their capacity still played a role - with a consistent increase in passenger traffic, they are still actively used by large airlines.

Historical dynamics of world passenger traffic

Toward the beginning of this century, the focus shifted towards the development of engines with greater fuel efficiency and the large-scale use of small regional aircraft with a capacity of about 120-180 seats - according to the forecasts of the vast majority of industry experts, the near future lies with them, and over the next twenty years, 70% of demand on the part of airlines, it will be for this class of aircraft. In total, the world's airlines now use about 22,000 passenger airliners, it is expected that this number will double by 2034, while the total demand will be about 38,000 aircraft.

Forecast of changes in the world fleet of passenger aircraft

Source: Boeing market review

Of this number, 16,000 will replace aging aircraft currently operated by airlines, and 22,000 will provide fleet growth in line with growing passenger traffic - analysts agree that in the next two decades, total passenger traffic will grow by more than two and a half times, and the lion's share of this increase will be for regional transportation, mainly in Asian countries.

Forecast of the dynamics of world passenger turnover

Source: United Aircraft Corporation market survey

The current market trend is mainly characterized by the effects of the liberalization of the air travel market, namely an increase in the number of airlines, increased competition and falling fares, which make flights more affordable and support passenger demand. Globalization is also an essential characteristic of the market today - the concepts of national companies are very vague, many carriers operate under code-share agreements, serving "group" flights with a transfer from one company's aircraft to another's aircraft within one air ticket. At the same time, the process of consolidation of companies is observed in developed markets - this applies to Europe, the United States, and Russia. At the same time, the boundaries between the price segments occupied by specific companies are gradually blurring - there is a convergence of traditional transportation and the low-cost format in the form of combined business models.

At the moment, the United States is the undisputed leader in terms of passenger traffic, not least due to the highest intensity of domestic traffic, due to the vast area, the relatively uniform location of large cities in the eastern part of the country, as well as the high degree of population mobility. In the list of ten airlines that became the world leaders in terms of passenger traffic in 2015, the 1st, 2nd, 3rd and 6th places are occupied by American carriers - American Airlines, Southwest Airlines, Delta Airlines and United Arilines, respectively.

Top 10 airlines by passenger turnover in 2015, bln pkm

In terms of air fleet by mid-2016, American companies do occupy the top five places - American Airlines with 1556 boards, Delta Air lines with 1330, United Airlines with 1229, Southwest Airlines with 720 and the world leader in air cargo transportation FedEx Express with 688. Thus Thus, it can be calculated that only the top five companies account for about a quarter of the entire global fleet. American Airlines, United Airlines and Delta Air lines also lead in the number of airports connected by the flights of these companies, however, in terms of the number of countries included in the route map, American carriers do not even fall into the top five - the leader is Turkish Airlines, which operates flights to 108 countries world, followed by the largest European airlines - Lufthansa, Air France and British Airways, closes the top five Qatar Airways.

Turning directly to the current state of the market, it makes sense first of all to note that there were two main factors that influenced the global demand dynamics in the last completed year - this is a gradually growing demand from the countries of the East and the continued collapse in oil prices. The fall in prices in the commodity market directly mediated the fall in the dollar cost of jet fuel, the cost of which is about a third of the total operating expenses of airlines. Due to their reduction, carriers were able to afford to reduce tariffs without loss of profitability, thus attracting new customers.

Aviation fuel cost dynamics

The aviation industry as an industry was formed in the early twentieth century. By 1910-12, in many countries there were several enterprises involved in the production of aircraft. Interest in the industry arose during the time of world wars, in particular, the Second World War, when air supremacy became one of the determining factors in a particular battle. After 1945, the industry continued to grow rapidly, during this period, paying more attention to civil aviation. By the end of the 80s, the aviation industry approached the modern model and then practically did not change its appearance. Currently, several leading countries of the aviation industry have formed in this sector, holding their positions.

Modern leaders - what are their features

Currently, the world leadership in the aviation industry belongs to several states, including: the USA, Russia, the EU and Brazil. These countries have the largest number of factories and plants operating in this industry. Some companies within the state can afford to produce single parts, but all of them eventually go to larger enterprises that form the basis of the national aircraft industry.

The peculiarities of the leading companies in the leading countries of the aviation industry is the fact that they all cooperate with the state. If we are talking about civil aviation, then this is servicing major carriers, national flights, and if we are talking about military aviation, it is meeting the needs of the armed forces.

Leading companies in the civil aviation industry

Civil aircraft industry is the most costly group, which includes only large enterprises with a narrow specialization of the national or international level.

In the civil aircraft industry today, two large corporations are leading:

- Boeing (American company);

- Airbus (United Corporation of the EU);

- United Aviation Corporation of Russia.

There are no enterprises of similar scale in other countries. A key feature of these companies is the dispersal of production throughout the country or several countries (EU). This approach allows you to sharpen production at one plant for the production of one part, drag factories to resources and, therefore, minimize production costs. In addition, these companies were able to appear only thanks to the merger of the giants. So, for example, the UAC includes several large enterprises "Su", "Mig", "Il", "Tu", "Yak", focused on general production.

Other major aviation companies in the world are: Lockheed Martin, Northrop Grumman, United Technologies, Textron (USA).

China is likely to become one of the leading aircraft manufacturers in the near future, but today its production cannot yet compete with the world's giants.

Military aviation

In the military sector, the leaders of the aviation industry look different. The following brands fall into this category:

- Su (made in Russia);

- Mig (Russia);

- Panavia Tornado (Germany);

- Eurofighter Typhoon (produced by the European Union);

- Boeing (combined US production).

In this sector, it is rather difficult to determine leadership between brands, since companies producing such equipment are reluctant to advertise their own sales. However, we can say with confidence that in this sector the top three remain unchanged: the US, the European Union and Russia. Interesting developments in this industry also belong to Israel, Canada, China and some other countries, but they are produced in a much more modest volume.

The global civil aircraft market is 90% “captured” by the American company Boeing and the European manufacturer Airbus. However, it seems that the hegemony of these companies will soon come to an end. Who is able to oust these titans? Which companies and countries are going to get involved in the fight?

The civil aircraft market is a global growth market without national borders and at the same time is characterized by fierce competition from national manufacturers. Difficult technological challenges and high costs mean that only a small number of countries and a few large companies operate in the aircraft industry. Thus, in the market of aircraft manufacturers, competition is oligopolistic in nature, i.e. dominated by a few large international companies that have the strongest influence on the entire market.

The leaders of the civil aviation industry in recent decades have been Boeing (USA) and Airbus (EC), occupying more than 90% of the global passenger aircraft market, but the technological development of the industry and the emerging demand patterns in the coming years will lead to the destruction of the already familiar duopoly of Western aircraft manufacturing giants. In this paper, we deliberately do not include in the analysis the plight of the domestic aviation industry, which was the subject of another article by the author (Tolkachev S.A. The new look of the domestic aviation industry / / Capital of the Country, 09/01/2010.), in order to consider in its purest form the hard the world market of civil airliners, where Russia has a place in the backyard after the inglorious surrender of positions (in fact, as in the First World War) as a result of the collapse of the USSR and the socialist bloc in 1989-1991. One of the forms of indemnity for the alleged “defeat” of the USSR in the Cold War with the West was the surrender to the “winners” of the gigantic civil aircraft market, estimated at that time at 40% of the world. As it will become clear from the further presentation, only on this “democratic” Russia, as the successor of the USSR, lost at least 1 trillion rubles in 20 years. dollars (!) or the total cost of oil exports for the same period. Therefore, to seriously approach the analysis of the world market for airliners with the participation of fragments of the mighty Soviet aviation industry, which today is timidly knocking on the door either with unfinished late Soviet developments (Tu-204, Tu-334, An-148), or with generic Western models (Sukhoi Superjet 100, MS-21), just do not want to.

1. The main segments of the civil airliner market

All civil aircraft produced in the world intended for the mass transportation of passengers are divided into the following segments depending on the type of fuselage and flight range:

1) medium and long-haul wide-body aircraft:

The fuselage diameter is from 5 to 6 meters. Aircraft with two aisles between the seats in the cabin. There are usually 7 to 10 passenger seats in a row. For comparison, narrow-body aircraft usually have a fuselage diameter of 3-4 meters. In the passenger cabin of a wide-body aircraft, the seats are arranged in 3-5 rows. On average, a wide-body aircraft can take on board 300-500 people.

The following wide-body aircraft are currently in operation (Table 1):

Table 1. Major wide-body aircraft in service.

| aircraft type | years of release | number of passengers | maximum range | total issued |

|---|---|---|---|---|

| A 300 | 1972-2007 | 270 | 7 000 | 561 |

| A 310 | 1982-1997 | 205-280 | 9 000 | 255 |

| IL-86 | 1980-1997 | 350 | 4 600 | 106 |

| MD-11 | 1988-2000 | 298-410 | 13 400 | 200 |

| In 747 | 1969-nv | 366-524 | 14 800 | 1 419 |

| In 767 | 1982-nv | 180-375 | 11 300 | 1 000 |

| A 340 | 1991-nv | 261-475 | 16 700 | 374 |

| IL-96 | 1993-nv | 300-436 | 12 000 | 29 |

| A 330 | 1994-nv | 255-295 | 13 000 | 671 |

| In 777 | 1994-nv | 301-451 | 17 500 | 901 |

| A 380 | 2007-nv | 525-963 | 15 400 | 60 |

| In 787 | 2009-nv | 210-350 | 16 300 | 7 |

| A 350 (project) | ---- | 270-412 | 15 700 | ----- |

2) medium and long-haul narrow-body aircraft:

The fuselage diameter is up to 4 meters. Compared to wide-body aircraft, narrow-body aircraft take on a much smaller number of passengers and, as a rule, have a shorter flight range. The maximum passenger capacity is 289 people.

Narrow-body aircraft in particular include (Table 2):

- Airbus A320 is the most massive European passenger jet aircraft.

- The Boeing 737 is the most massive passenger jet in the world.

- IL-62 is a narrow-body aircraft with the longest flight range.

- Tu-154 - the most massive Soviet passenger jet aircraft,

Table 2. Major narrow-body aircraft in service.

| Aircraft type | Release years | Passengers | Maximum range | Total Issued |

|---|---|---|---|---|

| Caravelle | 1959-2005 | 104-130 | 1 800 | 285 |

| IL-62 | 1966-2010 | 186 | 11 000 | 277 |

| Tu-154 | 1968-2011 | 150-180 | 3 500 | 1 020 |

| Yak-42 (142) | 1977-2002 | 100-120 | 4 000 | 188 |

| MD-80 | 1980-1998 | 140-172 | 4 500 | 1 191 |

| In 757 | 1982-2004 | 200-280 | 7 200 | 1 050 |

| B 717 (MD95) | 1998-2006 | 98-106 | 3 800 | 156 |

| In 737 | 1968-nv | 85-215 | 6 000 | 6 285 |

| A 320 (318/319) | 1987-nv | 107-220 | 6 500 | 4 181 |

| Tu-204 | 1990-nv | 164-212 | 7 500 | 66 |

| Tu-334 | 2000-nv | 102-138 | 4 100 | 5 (test) |

| Embraer ERJ 195X | 2006-nv | 106-118 | 3 990 | n/a |

| Bombardier CSeries | plan 2013 | 100-150 | 5 500 | --- |

| MS-21 (project) | plan 2016 | 150-212 | 5 500 | --- |

| COMAC С919 (project) | plan 2014 | 168-190 | n/a | --- |

3) regional jets:

Regional aircraft include even smaller aircraft. They carry up to 100 passengers over distances of up to 2-3 thousand kilometers. These aircraft can be equipped with both turboprop and turbojet engines. These aircraft include aircraft of the ERJ, CRJ, ATR, Dash-8 and SAAB families (Table 3).

Table 3. Main types of regional aircraft in service.

| Aircraft type | Release years | Passengers | Maximum range | Total Issued |

|---|---|---|---|---|

| An-24 | 1962-1979 | 48 | 1 000 | 1367 |

| Yak-40 | 1966-1981 | 27-36 | 1 300 | 1013 |

| BAe 146/Avro RJ | 1987-2003 | 85-100 | 2 000 | 387 |

| Fokker 100 | 1986-1997 | 85-119 | 3 100 | 238 |

| An-28 (An-38) | 1969-nv | 18-27 | 900 | 191 |

| Bombardier DHC-8 (series) | 1984-nv | 37-78 | 2 500 | 844 for 2008 |

| ATR 42 | 1984-nv | 40-50 | 1 500 | 390 |

| ATR 72 | 1989-nv | 50-75 | 1 300 | 408 |

| Bombardier CRJ (series) | 1991-nv | 50-100 | 3 800 | 533 |

| Embraer ERJ 145 (series) | 1999-nv | 35-50 | 3 000 | 1000 for 2007 |

| An-140 | 1999-nv | 52 | 2 400 | 12 |

| IL-114 | 2001-nv | 64 | 1 500 | 16 |

| Embraer E-Jet (series) | 2002-nv | 78-100 | 4 600 | 660 |

| Sukhoi Superjet 100 | 2008-nv | 68-98 (130) | 4 500 | 8 |

| An-148 (158) | 2009-nv | 70-99 | 6 200 | 13 |

| ARJ21 (China) | 2008 | 70-100 | 3 700 | 1 (experience) |

| MitsubishiRegionalJet (project) | 2014 plan | 70-90 | 3 000 | --- |

| Tu-324 (414) project | there is no data | 52-76 | 3 500 | --- |

4) local planes:

The smallest class of passenger aircraft are local aircraft designed to carry a small number of passengers (from 20) over distances up to 1000 kilometers. They are most often equipped with turboprop or piston engines. The most common aircraft of this class are produced by Cessna and Beechcraft.

For a better understanding, we present a comparative table 4, which includes all segments of civil airliners.

Table 4. Segments of the passenger aircraft market and their predicted capacity (in kind and value) for the period 2005-2024

2. The main companies participating in the civil airliner market

The passenger aircraft market has historically been dominated by American and European manufacturers. Boeing and Airbus are the largest civil aircraft manufacturers in the world.

Airbus S.A.S. (pronounced Airbus) - one of the largest aircraft manufacturing companies, produces passenger, cargo and military transport aircraft of the same name. The company headquarters is located in Toulouse, France. In 2001, according to French law, it was merged into a joint-stock company or "S.A.S." (French Société par Actions Simplifiée - simplified joint stock company). Airbus' sole shareholder is EADS. Airbus employs about 50 thousand people and is concentrated mainly in four European countries: France, Germany, Great Britain, Spain. The final assembly of products is carried out at the company's factories in the cities of Toulouse (France) and Hamburg (Germany).

Airbus' civil aircraft lineup began with the twin-engine A300. A shortened version of the A300 is known as the A310. Building on the lack of success of the A300, Airbus began developing the A320 project with an innovative fly-by-wire control system. The A320 was a big commercial success for the company. The A318 and A319 are shortened versions of the A320 offered by Airbus for the corporate jet market (AirbusCorporateJet) with some modifications. A stretched version of the A320 is known as the A321 and competes with later Boeing 737s.

Inspired by the success of the A320 family, Airbus decided to develop a family of even larger airliners. This is how the twin-engine A330 and the four-engine A340 were born. One of the key features of the new aircraft is the new wing design, which has a large relative thickness, which increases its structural efficiency and internal fuel volumes. The Airbus A340-500 has a range of 16,700 kilometers, the second longest-range commercial jet after the Boeing 777-200LR (17,446 km).

The company is particularly proud of its own fly-by-wire technology, unified cockpit and on-board systems used in all aircraft families of its own design; they make crew training and retraining to new models much easier.

The latest development of the company A350XWB is designed to compete with Boeing's new model - 787.

The Boeing Company- one of the world's largest manufacturers of aviation, space and military equipment.

The headquarters is located in Chicago (Illinois, USA).

The main production facilities of the company are located in the cities of Everett (Washington), California, St. Louis (Missouri).

The company produces a wide range of civil and military aviation equipment, being, along with Airbus, the largest aircraft manufacturer in the world. In addition, Boeing produces a wide range of military aerospace equipment (including helicopters), conducts large-scale space programs (for example, the CST-100 spacecraft).

The company's factories are located in 67 countries around the world. The company supplies its products to 145 countries of the world. Boeing works with more than 5,200 suppliers in 100 countries.

In 2001, a division of Boeing International was formed, which controls the company's work in 70 countries of the world, except for the US market, where it is responsible for the development and implementation of the company's global development strategy. It determines and evaluates the competitive advantages and opportunities in the host country for the development of intellectual resources and technologies, the development of partnerships and business.

3. Comparative characteristics of the release of Airbus and Boeing

The companies operate mainly in the segments of narrow-body and wide-body short- and medium-haul aircraft.

Below is a comparative description of the release of certain aircraft models by year.

- ? B-737 and A320. Medium-capacity aircraft for medium-haul airlines, each type has many modifications. In recent years, A320s have been sold in larger volumes than Boeing products.

Table 5. Deliveries of AirbusA320 and Boeing 737 for 1988-2010

| 2010 | 2009 | 2008 | 2007 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| A320 | 401 | 402 | 386 | 367 | 339 | 289 | 233 | 232 | 236 | 257 | 241 |

| B-737 | 398 | 372 | 290 | 330 | 302 | 212 | 202 | 173 | 223 | 299 | 281 |

| 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | 1993 | 1992 | 1991 | 1990 | 1989 | 1988 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A320 | 222 | 168 | 127 | 72 | 56 | 64 | 71 | 111 | 119 | 58 | 58 | 16 |

| B-737 | 320 | 281 | 135 | 76 | 89 | 121 | 152 | 218 | 215 | 174 | 146 | 165 |

- B-747 and A380. Large capacity aircraft for medium and long haul airlines. Asian airlines, traditional users of the 747, are the main customers of the A380. Currently, B-747s are produced in quantities of no more than 10 pieces per year, there are very few new orders for passenger cars (out of 99 B-747s ordered since the beginning of 2006, only 27 are passenger ones). At the same time, the A380 order book has increased by 60 passenger liners since the beginning of 2006.

- B-767 and A330. The Airbus aircraft has proved commercially more successful in recent years.

Table 6. Deliveries of Airbus A330 and Boeing 767 aircraft in 1994-2009

| 2009 | 2008 | 2007 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A330 | 78 | 72 | 68 | 62 | 56 | 47 | 31 | 42 | 35 | 43 | 44 | 23 | 14 | 10 | 30 | 9 |

| B-767 | 13 | 9 | 12 | 12 | 10 | 9 | 24 | 35 | 40 | 44 | 44 | 47 | 42 | 43 | 37 | 41 |

- B-777 and A340. Both aircraft appeared at the same time, but due to the greater fuel efficiency of the B-777 and a number of other factors, the American company sold twice as many aircraft as their European competitors.

Table 7. Deliveries of Airbus A340 and Boeing 777 for 1993-2009

| 2009 | 2008 | 2007 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 1996 | 1995 | 1994 | 1993 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| B-777 | 88 | 61 | 75 | 65 | 40 | 36 | 39 | 47 | 61 | 55 | 83 | 74 | 59 | 32 | 13 | 0 | 0 |

| A-340 | 8 | 13 | 11 | 24 | 24 | 28 | 33 | 16 | 22 | 19 | 20 | 24 | 33 | 28 | 19 | 25 | 22 |

There are very few new orders for the A340. It is assumed that the A350 will compete with the B-777, but the development of the latter is still very far from complete.

Embraer (Empresa Brasileirade Aeronautica) is a Brazilian aircraft manufacturing company, one of the leaders in the global market for passenger regional aircraft. Headquartered in Sao José dos Campos, State of Sao Paulo.

Founded in 1969 as a government controlled company. In the 1990s, it faced a serious crisis, after which it was completely privatized in 1994 (the state had only a “golden share”, which gives it the right to veto in the supply of military aircraft).

The company specializes in regional liners and produces commercial, corporate, military, agricultural aircraft. Production facilities are concentrated in Brazil.

By 2010, the company shared third or fourth place with the Canadian Bombardier among the largest suppliers of commercial airliners, behind Boeing and Airbus. In 2009, the company delivered more than 240 aircraft to commercial customers.

The number of personnel is 17 thousand people (2005).

Embraer Jet - a family of twin-engine narrow-body medium-range passenger aircraft manufactured by the Brazilian company Embraer. Includes 4 modifications: E-170, E-175, E-190 and E-195. The E-Jet was first presented at the Le Bourget Air Show in 1999. Serial production began in 2002.

Table 8. Deliveries of Embraer E-jet 190, 195 aircraft in total for 2005-2010, pcs.

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

|---|---|---|---|---|---|

| 39 | 37 | 32 | 52 | 33 | 23 |

bombardier inc. (Bombardier), a Canadian engineering company. The headquarters is located in Montreal, Quebec.

The company was founded in Valcourt (Quebec) in 1942 under the name L´Auto-NeigeBombardierLimitée by Joseph-Armand Bombardier. The company has been engaged in aircraft construction since the mid-1980s. In 2003, the company sold its snowmobile, all-terrain vehicle, jet ski, powerboat division to Bombardier Recreational Products, concentrating on rail and aircraft engineering.

The company is one of the world's largest manufacturers of business jets, regional aircraft, as well as railway equipment and trams. The main divisions of the company are the world's largest manufacturer of railway equipment Bombardier Transportation and Bombardier Aerospace, the world's third largest manufacturer of civil aircraft after Boeing and Airbus. In 2008, Bombardier employed 59.8 thousand people.

Bombardier Canadair RegionalJet (CRJ) is a family of regional passenger jet narrow-body aircraft. The aircraft made its first flight on May 10, 1991. The CRJ-100 became the first aircraft of the modern level among the 50-seat aircraft. In terms of speed, the aircraft can be compared with larger machines, while its efficiency is quite consistent with the class. The family consists of several modifications that differ in fuselage length and flight range: CRJ100, CRJ 200, CRJ 700, CRJ 900.

The CRJ 900 model is designed to carry 88 passengers. The Bombardier CRJ 900 made its first flight on February 21, 2001. In addition to the standard, there are several more versions of the aircraft - elongated and for long-distance flights.

The Bombardier CRJ 1000 program was launched by Bombardier Aerospace on February 19, 2007. First flown in September 2008, the 100-seat CRJ1000 is the latest model in the Canadian Regional Jet family.

Table 9. Deliveries of Bombardier CRJ 900, 1000 aircraft in 2005-2010, pcs.

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

|---|---|---|---|---|---|

| 57 | 48 | 78 | 92 | 82 | 87 |

4. Growth forecasts for the global civil airliner market

According to Airbus forecasts, in the next 20 years, airlines around the world will buy almost 25,000 new long-haul aircraft for a total of 2.9 trillion. dollars. Of these, about 10,000 will be required to replace the aging fleet, and another 15,000 will be needed to further increase the carrying capacity. Moreover, it is narrow-body airliners that will be in the greatest demand. They will be sold about 18 thousand for 1.27 trillion. dollars, which will be 70% of the total volume of all deliveries in physical terms. As a result, by 2030 the global airline fleet will almost double and exceed 30,000 aircraft. High demand for new aircraft is driven by the growing need to replace airliners with low fuel efficiency, as well as the dynamic development of new markets and the growth of passenger traffic on existing routes.

Boeing predicts that the new civil aircraft market will be worth $3.6 trillion over the next 20 years. dollars Market growth will be accompanied by the recovery of the global economy after the crisis and an increase in demand for new and more efficient aircraft. According to the current 2011 market review, by 2029 the market capacity will be 30,900 new passenger and cargo aircraft.

Table 10. Future market value (at 2009 prices) and aircraft deliveries by region by 2029

| Region | Market value of deliveries in billions of dollars | Aircraft deliveries, pcs. |

|---|---|---|

| Pacific Asia | 1 320 | 10 320 |

| North America | 700 | 7 200 |

| Europe | 800 | 7 190 |

| Near East | 390 | 2 340 |

| Latin America | 210 | 2 180 |

| CIS | 90 | 960 |

| Africa | 80 | 710 |

| Total | 3 590 | 30 900 |

The table shows that in the long term, the volume of passenger traffic will increase by 5.3% per year under the influence of economic growth in regions with different patterns of demand for aircraft. The fastest growing segment of the global market will continue to be narrow-body aircraft, thanks to the explosion of low-cost airlines, the development of new markets such as India, China and Southeast Asia, and continued volatility in fuel prices. The growth rate of the narrow-body aircraft segment has outpaced the wide-body segment over the past ten years. This gap will continue to widen as older aircraft are phased out of the airline fleet.

The highest growth rates are observed in the Asia-Pacific region, in which China is the undisputed leader.

Today, this region provides about 1/3 of the world's air traffic. As a result of the growth of this market, by 2029 the Asia-Pacific region will account for almost 43% of inbound, outbound and domestic traffic. China alone will need 4,300 new airliners over the next 20 years.

Local airlines will also be the most active buyers of wide-body aircraft, generating about 40% of total demand.

Another dynamic market is the Middle East, which has seen one of the highest air traffic growth rates in recent years. Middle East airlines have achieved rapid growth by taking advantage of their geographic location, the demographics of the region, the acquisition of modern aircraft, and well-thought-out investment and business development plans. To the Middle East for the period 2011-2029. 2340 aircraft will be delivered.

The following table provides more detailed data on the distribution of deliveries of different types of airliners by major regions.

Table 11. Aircraft Deliveries by Region by Size, 2011-2029

| Region | Regional (pcs.) | With one pass (pcs.) | With two passes (pcs.) | Large (pcs.) | Total (pcs.) |

|---|---|---|---|---|---|

| Pacific-Asian region | 470 | 6 710 | 2 840 | 300 | 10 320 |

| North America | 800 | 5 180 | 1 180 | 40 | 7 200 |

| Europe | 310 | 5 380 | 1 340 | 160 | 7 190 |

| Near East | 70 | 1 100 | 1 000 | 170 | 2 340 |

| Latin America | 20 | 1 800 | 350 | 10 | 2 180 |

| CIS | 200 | 570 | 160 | 30 | 960 |

| Africa | 50 | 420 | 230 | 10 | 710 |

| Total | 1 920 | 21 160 | 7 100 | 720 | 30 900 |

5. Increasing competition and the end of the duopoly

Airbus and Boeing's portfolio of firm orders for narrow-body aircraft is now approaching 3,000 units, which is only 16% of the forecast demand for these liners over a twenty-year period. Thus, the world market for long-haul aircraft has all the prerequisites for the emergence of at least one more major player, which, under certain circumstances, may well press the giants of the world aircraft industry. The duopoly is slowly coming to an end. Of all the aircraft manufacturers in the world, the challenge to the "Big Two" - Airbus and Boeing - was the first to be thrown by Canadians. Five years ago, Bombardier made the decision to start developing the C-Series narrow-body aircraft, designed to carry 110-130 passengers. Initially, the implementation of this project was hampered by the intractability of aircraft engine manufacturers, who, according to some experts, being under pressure from Airbus and Boeing, did not show a desire to create new engine modifications specifically for the new Bombardier aircraft. They motivated their decision by the narrowness of the sales market. But thanks to the efforts of the Canadian authorities and the position of Pratt & Whitney Canada, as well as the changing market situation, this problem was eventually resolved. Having received financial support from the province of Quebec, Pratt & Whitney nevertheless developed a new family of Pure Power engines. These are exactly the units that Irkut will use on its MS-21. But unlike the MS-21 program, the C-Series project has already gone more than half way. In the middle of last year, Bombardier presented working drawings of the SC100 test aircraft, and the final design of the left fuselage skin was shown at the Saint-Laurent plant in Montreal. Now at this enterprise, the installation of composite panels on the tail section of the liner is already in full swing.

The new aircraft should take to the air in 2012, and the first deliveries of the liner to airlines are scheduled for 2013. But, despite all the advantages of the new liners, Bombardier still cannot boast of a large portfolio of orders for them: Canadians have only 90 firm contracts for the purchase of the SC100 and the same number of options. The main customers of these aircraft are the Lufthansa Group, the Irish leasing company LCI and the American Republic Holdings. But Bombardier pins its main hopes on the Chinese market. According to the forecasts of the Canadian company, within the next 20 years it will become the second largest market for commercial aviation. To achieve this goal, the company decided to cooperate with Chinese aircraft manufacturing enterprises.

China has its own project for the creation of a mainline narrow-body aircraft - C919. And this project is nothing but China's long-term plan to destroy the Airbus and Boeing duopoly. The name of the model and its digital code for the Chinese have a great symbolic meaning. The first number "9" can be interpreted as "a long time to overcome a difficult path", and "19" means that the first Chinese long-haul aircraft will be able to carry 190 passengers. In addition to the basic version, the Commercial Aircraft Corporation of China (COMAC) has begun designing two more models - for 156 and 168 passengers.

Within a few months, COMAC expects to complete the overall technical design of the aircraft and select suppliers of all key systems. This process has been actively going on for the last year and a half.

COMAC plans that the first flight of the C919 should take place in 2014, and the commercial operation of the liner will begin in 2016. In total, the Chinese intend to produce 2,500 new aircraft within 20 years. True, COMAC has not yet paid firm orders for the C919. But there is no doubt that they will appear in the near future.

The expansion of three new manufacturers of long-haul aircraft to the market at once forced Airbus and Boeing to begin full-scale preparations to repel the attack. Airbus has decided to launch a remotorization program for the A320 family, which, after being equipped with new engines, will be called NEO. The European concern intends to invest about 1 billion euros in this project. It is planned to install all the same engines of the LEAP-X and PurePower families on new aircraft. Moreover, Airbus is going to equip its upgraded airliners with new wingtips, which will further reduce fuel consumption by 3-4%. Thus, the total fuel savings will be about 18%. The design of the A320 NEO airframe is 95% similar to the currently operated aircraft of this family. The European concern will have to strengthen only the wing and pylons. The remotorized aircraft will hit the market as early as 2016 and will cost just $6 million more than their predecessors. In total, Airbus is going to sell about 4,000 A320 NEOs. And it is not excluded that this plan will be fulfilled sooner or later. In a month and a half of sales, Airbus has already acquired three major customers. The launch customer for the A320 NEO was Virgin America, which signed a contract for the purchase of 30 aircraft. India's IndiGo and Malaysia's AirAsia soon followed suit with tentative agreements to purchase more than 200 new aircraft. This sent EADS (the parent company of Airbus) shares up 5% on the day. The company's management is confident that the residual value of the existing A320 models will not suffer much, but the newly minted competitors of the European concern will have a hard time.

Boeing considered the launch of the NEO project a belated response to its Next Generation family of aircraft, which have been in production for more than a decade. At the same time, Boeing intends to create a new family of aircraft in the near future to replace the existing versions of the Boeing 737 NG. The company understands Airbus's expectations from the release of the new NEO model, but does not see the need for such liners, the company's strategy, in accordance with the expectations of its customers, is aimed at designing a new aircraft.

The Brazilian Embraer is also considering the possibility of creating a new mainline aircraft for 110-130 passengers. The company is waiting for Boeing to make a final decision on the release of its new airliner, and even then it will consider whether they should take on a competing project.

***

The modern aviation industry is a global network of thousands of specialized suppliers of various components and manufacturing services located around the world, incl. and in Russia.

The current state of the aviation industry market is characterized by a stage of stabilization. It is characterized by an established mature market for the products of the relevant industry. This means that the aviation industry market is segmented:

- medium and long-haul wide-body aircraft;

- medium and long-haul narrow-body aircraft;

- regional jets;

- local planes.

An important feature of the state of the civil airliner market today is the continuous increase in the role of innovation to achieve success: a change in the situation in the external environment requires a review of the role and place of innovation in the activities of companies. An analysis of the development trend of the world market in the 20th century revealed the main feature: the development of the market is a continuous increase in volatility, instability and unpredictability.

The basis of the development strategies of the world's leading civil aircraft manufacturers is the continuous technological improvement of their products and the reduction of operating costs of the proposed aircraft models, including fuel consumption and repair and maintenance costs, as well as the development of deep and long-term relationships with airlines by providing them with comprehensive support in operation. , modernization and renewal of the aircraft fleet. At the present stage, the range of products manufactured by Boeing and Airbus, as well as Embraer and Bombardier, is largely similar when compared in terms of such characteristics as the size, range and cost of the aircraft.